Here are the most and least expensive states for car insurance, and why rates vary

Where you live can matter more than how you drive. A Louisiana driver with a spotless record pays nearly 2.5 times more than an identical driver in Vermont — not because they're a bigger risk behind the wheel, but simply because of the state on their driver’s license.

CarInsurance.com analyzed rate data for all 50 states and Washington, D.C., revealing just how wide that gap has become in 2026. The national average annual premium for a full-coverage policy now costs $2,578, but individual state averages range from $1,660 to $3,999, a difference of $2,339 per year.

"Most drivers don't realize how much their state's laws and local risk factors shape their premiums. Two drivers with identical records and vehicles can pay different rates simply because they live in different areas. Understanding your state's landscape is the first step toward making a confident insurance decision," said Brent Buell, lead data analyst at CarInsurance.com.

Key Insights: Most and least expensive car insurance states

- Vermont, New Hampshire and Hawai'i are the cheapest states for car insurance, according to a recent analysis by CarInsurance.com.

- Louisiana, Michigan and Nevada are three of the top 10 most expensive states for auto insurance. Insurance rates in Louisiana are $3,999 annually — 141% more than the cheapest state, Vermont.

- State laws, weather risk, uninsured driver rates and population density drive the biggest differences in what drivers pay for insurance in their state.

- Car insurance premiums nationwide increased by 23% since 2023, with New Jersey and Washington seeing the steepest increases — 57% and 51%, respectively.

- Comparing quotes from multiple insurers regularly is the most effective way for drivers to lower costs.

Average car insurance rates by state

On average, car insurance costs $2,578 a year for a full coverage policy with limits of 100/300/100 and $500 collision and comprehensive deductibles. However, this cost varies by state and other factors.

Every state has its own car insurance laws and requirements, and that's one reason why car insurance rates vary dramatically.

Additionally, auto insurers assign risk levels to ZIP codes based on the number of uninsured drivers and the frequency of thefts, collisions and vandalism to gauge the likelihood of such incidents in an area.

See the table below for average full-coverage car insurance rates by state.

CarInsurance.com

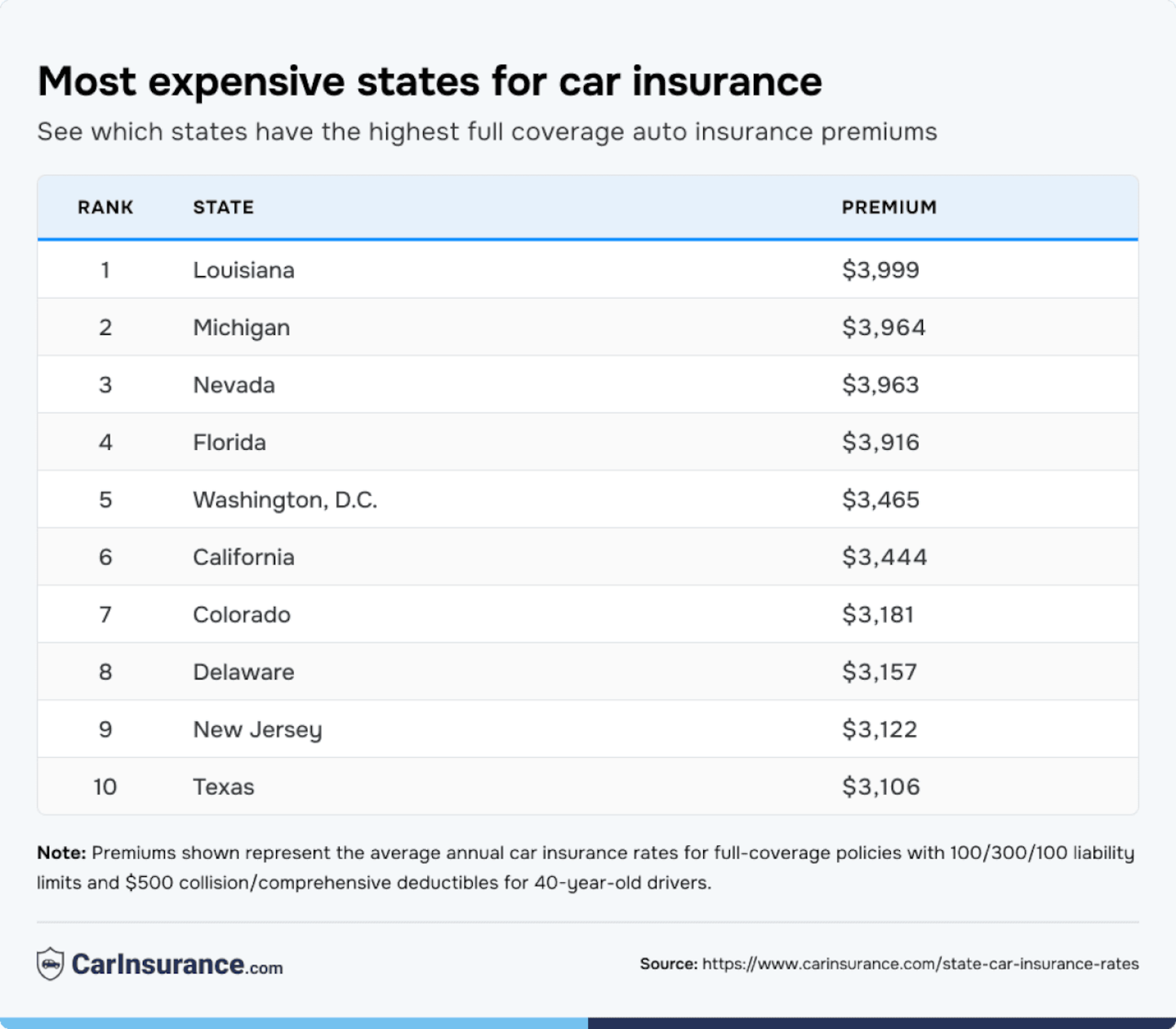

States with the most expensive auto insurance rates

Louisiana ($3,999), Michigan ($3,964), Nevada ($3,963), Florida ($3,916) and Washington, D.C. ($3,465) are the most expensive states for car insurance in the U.S.

Mark Friedlander, senior director of media relations for the Insurance Information Institute in St. Johns, Florida, said Florida rates are driven by severe weather and uninsured motorists.

“Florida drivers pay high average premiums in the United States due to a variety of factors,” Friedlander said. “These include the impact of severe weather on roadways, heavy traffic patterns on interstates generated by residents and millions of annual visitors, congested roadways in major metro areas, a state’s no-fault insurance law … and the fact that Florida has one of the highest uninsured motorist rates in the United States — 20.4%.”

Based on CarInsurance.com’s research, the table below shows the 10 states where average annual full coverage car insurance rates are the most expensive:

CarInsurance.com

States with the cheapest car insurance rates

Vermont offers the lowest average annual premium at $1,660, 36% below the national average. Other states with the cheapest rates include New Hampshire ($1,689), Hawai'i ($1,757), Ohio ($1,783) and Maine ($1,808).

“States that have the lowest overall car insurance premiums on average may have lower populations, which result in fewer car accidents and less money paid out by insurance companies, resulting in cheaper insurance premiums,” said Lauren McKenzie, an insurance broker at A Plus Insurance in Liberty, South Carolina.

See the states with the cheapest full coverage car insurance in the table below.

CarInsurance.com

Why car insurance rates vary by state

Car insurance rates aren’t just about your driving record — where you live can play an even bigger role. Each state sets its own rules for required coverage, liability limits and claims handling, all of which affect how much drivers pay.

Here are the biggest reasons rates differ from state to state:

- State coverage requirements: Some states require only basic liability coverage, while others mandate additional protections, such as uninsured motorist or personal injury protection (PIP). States' liability requirements also vary, and those with higher minimums naturally see higher average premiums. In January 2026, New Jersey raised its minimum auto insurance liability coverage limits to 35/70/25.

- Population density and traffic: Urban areas with higher traffic and more densely populated cities, such as New York and California, tend to have more accidents and higher insurance costs than rural states like Vermont and Maine.

- Weather and natural disasters: States prone to severe weather like hurricanes, floods or hailstorms, including Florida and Louisiana, experience higher claim volumes and repair costs, driving up premiums.

- Uninsured drivers: When more people on the road are uninsured, insured drivers end up paying more to cover that risk. For instance, Florida and Mississippi consistently rank among the states with the highest uninsured motorist rates.

- Repair and medical costs: Regional labor, medical care and parts pricing also impact premiums. States with higher healthcare or body shop costs tend to have higher full coverage premiums.

Did you know?

Even two neighboring states can have dramatically different insurance costs because of state laws and claims costs. Crossing from Vermont ($1,660/year) into New York ($2,596/year) nearly doubles the average annual premium in 2026.

Does population density affect insurance rates in your state?

Where you live is a crucial factor in determining how much you'll pay for car insurance, and the population in your state can affect your rates.

“On average, drivers in more sparsely-populated states such as Idaho and North Dakota are going to pay much less for coverage than drivers in more populous states such as California, Florida and New York,” Friedlander said. “But it goes beyond just the state you live in. Insurers determine rates by the city you live in and even your specific ZIP code. Traffic volume, accident frequency and severity, as well as theft and vandalism data, vary in every city throughout every state.”

In other words, you could live in a large metro like Los Angeles or Chicago and pay significantly different rates based on your ZIP code within that city. Urban drivers generally pay much more for auto insurance than rural drivers in the same state.

“If you live in an area with a high crime rate, a large number of accidents and large payouts, insurance prices will be higher there,” McKenzie said. “If you live in a state with busy, expensive cities where gas prices and rent costs are high, car insurance prices will be high as well.”

How much have car insurance rates increased over time?

Car insurance costs have climbed sharply nationwide in recent years, with nearly every state seeing double-digit percentage increases. The average jump across the U.S. was roughly 23%, reflecting continued inflation in repair costs, rising claim severity and weather-related losses.

More than 45 states experienced double-digit increases over the past two years, and 14 states saw increases of 30% or higher.

The most significant overall increases from 2023-26 occurred in:

- New Jersey: 57%

- Washington: 51%

- District of Columbia: 50%

- Idaho: 44%

- Vermont: 39%

These states posted increases between 39% and 57%, the highest in the nation.

On the other end of the spectrum, Alabama (5%), Montana (6%), South Dakota (6%), Missouri (10%) and Arizona (10%) saw the smallest increases, all increases of less than 10% or less. These states have lower population density, fewer catastrophic weather events and historically stable claim patterns. Overall, the data show that insurance affordability continues to diverge regionally.

Is your state a tort or no-fault state? See why it makes a difference

State laws vary when it comes to who pays for damages; most states are either tort or no-fault states.

In general, car insurance is more expensive in no-fault states because no-fault insurance law states that you do not need to prove who was at fault to receive compensation from your insurance company. In a no-fault state, each driver's insurance covers their medical expenses and lost wages after an accident, regardless of who is at fault. This system limits the ability to sue the other driver, except in cases of severe injury or significant damage.

On the other hand, if you cause an accident in a tort state (at-fault state), your insurance company will be on the hook for any damage/injuries you’ve caused. A tort state is one in which the driver found at fault in an accident is responsible for covering the other party's property damages and injuries.

Generally, this means the at-fault driver’s insurance company pays for the other parties' damages and medical costs. This system allows the injured party to sue the at-fault driver for compensation beyond what insurance covers.

How to find cheaper car insurance in your state

Even if your state’s average rate is above the national average, you still have options to save. Most drivers can lower their premiums with smart shopping and a few simple policy adjustments.

Compare quotes from multiple companies

Car insurance rates can vary by hundreds of dollars — even for the same coverage. Compare quotes from at least three insurers to find the best deal.

If you're unsure whether you're paying more than average, a car insurance calculator can help. By entering your ZIP code and age, you can see estimated rates in your area and compare them with how much you currently pay.

Adjust your coverage

If your car is older or paid off, you might save money by reducing optional coverages, such as collision or comprehensive. Just make sure you maintain enough protection to meet state laws and your financial comfort level.

Take advantage of discounts

Combine your auto and home or renters insurance policies with the same provider to qualify for multi-policy discounts that can save you up to 14%.

Also ask about:

- Savings for students earning good grades: 12%

- Usage-based or telematics programs (e.g., Drive Safe, Snapshot): 10%

- Defensive driving course credits: 5%

- Paperless billing: 3%

Review your policy regularly

Rates and life circumstances change. Reshop your policy every six to 12 months to ensure you’re still getting the best price. Even if you’re staying with the same insurer, updating your mileage or asking about discounts can reduce costs. Drivers who compare quotes annually can save an average of $1,245 or more per year, depending on their state and driving profile.

Minimum liability insurance requirements by state

Car insurance requirements and costs differ from state to state. Each state sets its minimum coverage limits, affecting how much drivers pay for basic liability insurance.

Some states require only liability coverage, while others mandate higher limits or additional coverages, such as personal injury protection (PIP) or uninsured motorist coverage.

Check the minimum car insurance requirements in your state and whether additional coverages, such as uninsured motorist protection or personal injury protection, are also required.

Frequently Asked Questions

Which states had the highest car insurance rate increases from 2023 to 2026?

New Jersey experienced the fastest increase at 57%, followed by Washington and the District of Columbia, at 51% and 50%, respectively. Other notable rises occurred in Idaho at 44%, Vermont (39%) and Maine (35%).

Which states had the lowest car insurance rate increases?

Alabama (5%), Montana (6%), South Dakota (6%), Missouri (10%) and Arizona (10%) recorded the slowest premium growth since 2023.

What’s the national average car insurance rate increase between 2023 and 2026?

Nationwide, car insurance premiums rose roughly 23% over three years. The increase reflects higher claim costs, expensive vehicle repairs, severe weather losses and inflation in both parts and labor.

Why did car insurance rates rise so much from 2023 to 2026?

Rates climbed due to several converging factors:

- Inflation: Higher prices for auto parts, repairs and medical care.

- Severe weather: More costly claims from storms, flooding and hail.

- Increased claim frequency and severity: More accidents and higher payouts.

- Rising reinsurance and legal costs: Insurers are passing some of these costs to consumers.

Which states now have the highest average car insurance costs?

The most expensive states are Louisiana ($3,999), Michigan ($3,964), Nevada ($3,963), Florida ($3,916) and Washington, D.C. ($3,465).

Which states have the cheapest average car insurance?

Vermont ($1,660), New Hampshire ($1,689), Hawai'i ($1,757), Ohio ($1,783) and Maine ($1,808) have the lowest average annual rates.

How important is it for car owners to shop around, and how often should they compare insurance rates?

You should shop around each time your policy renews. If you opt for a six-month policy, compare car insurance quotes from multiple insurance companies before signing up for another six months. Finding the lowest car insurance rates can lead to big savings.

What advice would you give drivers in states with high insurance rates to help them reduce their premiums?

"For those in states with high insurance rates, understanding the factors affecting their premiums is a must," said Scott Distasio, a Florida-based board-certified civil trial lawyer with extensive experience in auto accident law. "Simple actions like regularly checking credit reports, enrolling in defensive driving courses or leveraging multi-policy discounts can yield significant savings."

This story was produced by CarInsurance.com and reviewed and distributed by Stacker.